![]() 5 minute read

5 minute read

A continent[nbsp]with the longest recession-free term in the world and the population of more than 24 million people is signaling the troubles. Australia’s development has slowed down due to Chinese crisis and enlarging real-estate bubble. Those are signs of a need to develop new skills of citizens and provide more innovative solutions for real-estate. Who and how can turn this situation upside down and benefit the development?

Calm before the

storm

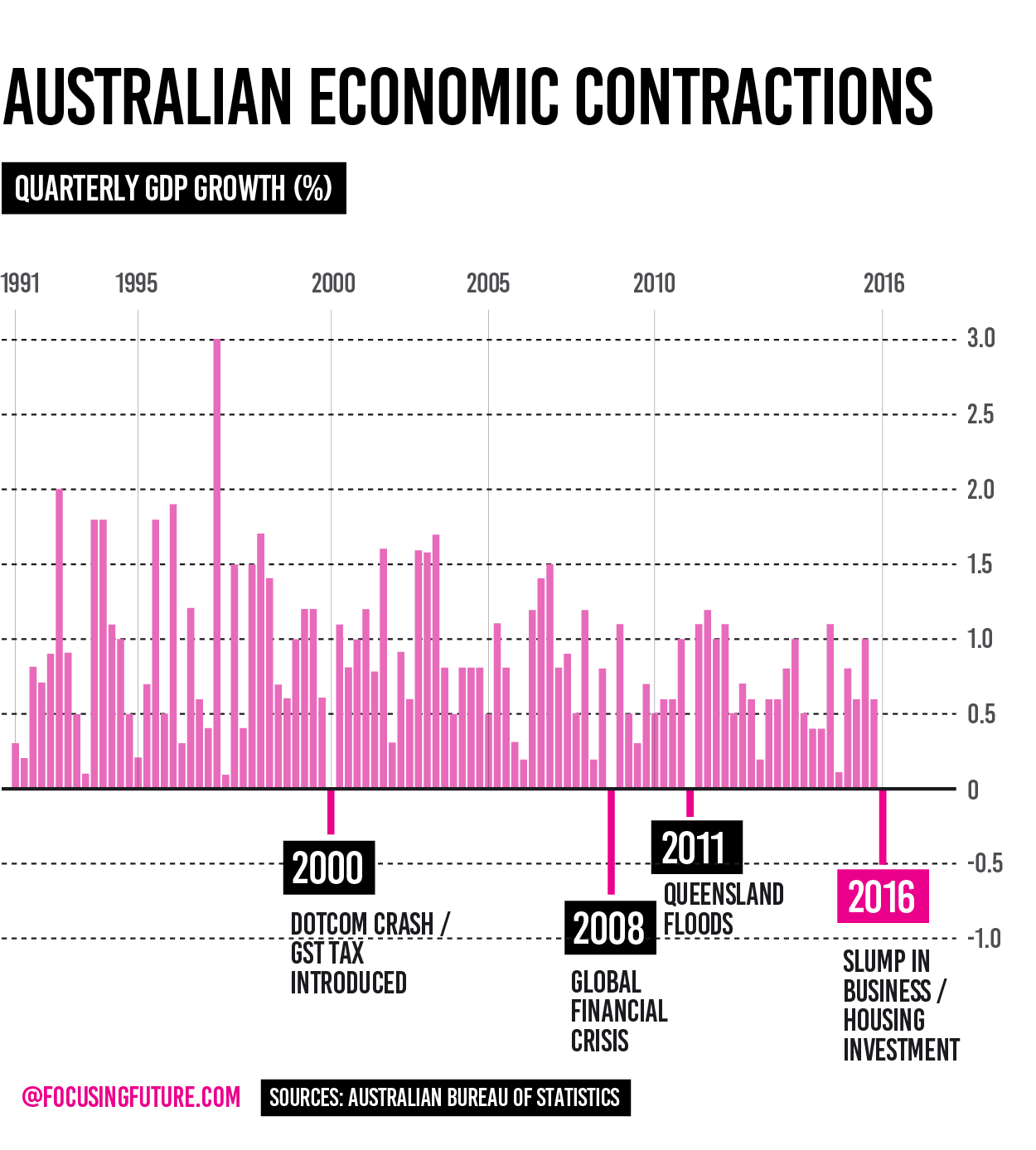

Australia had a continuous recession-free growth for a quarter of the century. A decade after a World Economic Crisis, Australia has reported the GDP plunge and contraction of new business investment 3.2 per cent. The drop has not been unexpected, however, the magnitude of the decline makes the result worthy of closer scrutiny. Deloitte Access Economics’ Chris Richardson has linked the Chinese crisis and ambiguous numbers: “Perhaps a better way to describe it is the numbers have been artificially good for a while and now they’re looking artificially bad. The bottom line is that for four years now, Australia’s economy has been growing just a little bit below trend and that’s partly because the boom in China has peaked. China has slowed and that is throwing some challenges our way.” Also, it has been suspected that China has been reporting increased GDP growth when numbers drastically fell in the beginning of 2016. Does the same problem arise in Australia as well?

The World Bank forecasts the stabilization of Australian economic in the next couple of years. As Daryl Dixon, executive chairman of Dixon Advisory, comments: “While Australian interest rates are unlikely to increase sharply in 2017, borrowing rates have bottomed with the major banks starting to increase fixed interest rates anticipating higher future rates. All things considered, 2017 could be a period of considerable uncertainty for both the property and the share markets.” Let’s get closer to investigate the gaps in property and real-estate markets.

Avocado vs

Housing

Autumn of 2016 was significant for a debate in Australia on the topic of overspending on smashed avocados and its impact on the inability to afford purchasing property. KPMG partner Bernard Salt in his column emphasized that millennials do not live to their income and fail to save money for the deposit on a house. The debate took a turn when calculations have proved that prices on real estate in Australia grow faster than salary and the chance to save enough for the first payment might not be worth to refuse from some delights of everyday life as avocado lunch once a week. One of the examples is a one-bedroom house in Sydney sold 3 times higher than it was in 2013 for $1,230,000.

Australian real-estate has demonstrated the challenge not only for millennials but also a huge impact of real estate bubble on the GDP growth. In the third quarter, new building investments have plunged for 11.5 percent. Moreover, according to Australian Bureau of Statistic, the value of construction fell by 3.5 percent due to delays caused by weather conditions. This signals a need of efficient building innovations that can help to deliver constructions on time and more effective social policies.

“The value of investment in residential building declined by 1.4 per cent in the quarter, however it remains 7.2 per cent higher than in the September quarter a year earlier. In the context of the residential building cycle reaching a record high, the decline in investment in the sector and the role that it played in the overall contraction in GDP is likely to be a point of discussion,” comments Geordan Murray, Housing Industry Association (HIA) Economist.

Moreover, the issue spreads for other generations as well. Aging of population is an important factor influencing the development of the sector for the next century. “Providing affordable shelter for our growing and aging population is the great political, social and economic challenge now and into the next decade,” stresses HIA Managing Director, Shane Goodwin. “Our national housing stock must provide choices for smaller family units, extended multigenerational households, mobile working families and our aging retirees alike. Providing these additional homes where they are needed and at an affordable price will require a cooperative partnership between governments, communities, regulators and industry.”

Developing

new habits

As absurd as Bernard Salt’s claim on lunch spendings versus savings for housing is, generations after baby boomers have to develop new skills and budgeting tools. Commonwealth Bank of Australia is on the list of most innovative Australian companies in 2016 for creating an app that is intended to lower the frustration with the home buying process. The app allows users to discover affordability of the property which would suit their lifestyle and financial position. At the same time, the app offers to assess estimated market price of the housing and apply for conditional eligibility loan. Bank empowers its clients to understand the process better by using an integrated calculator to determine borrowing power, repayments, and upfront costs. The significant benefit of this application is that it links real-estate market with the financial position of a user. This approach enhances and secures financial well-being of customers and communities. There is a hope that educating population budgeting skills will make them more aware of the choices, as well as, will rise a well-educated electorate for upcoming decades.